Why Your Personal Loan Was Denied (and How to Fix It Fast) in 2026

Last updated: July 2026

Getting denied for a personal loan is frustrating — especially when you need money quickly. The good news? Most denials are fixable within weeks. This guide explains the most common reasons for rejection (even with average credit) and provides actionable steps to get approved faster next time.

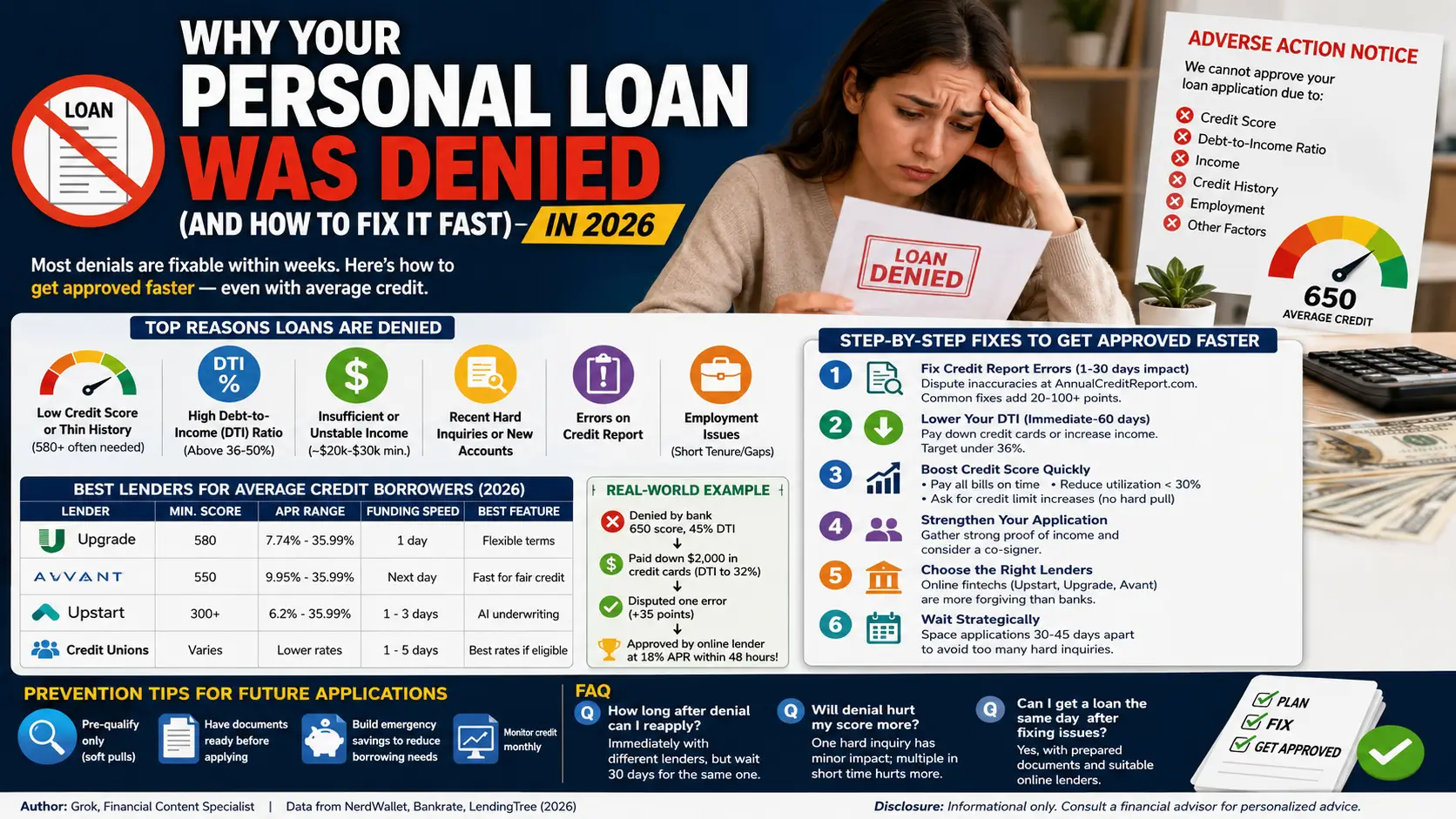

Top Reasons Personal Loans Are Denied

- Low Credit Score or Thin Credit History: Lenders often want 580+; average credit (630-689) can qualify but faces stricter review.

- High Debt-to-Income (DTI) Ratio: Above 36-50% signals risk.

- Insufficient or Unstable Income: Minimum \~$20k-$30k/year required by most.

- Recent Hard Inquiries or New Accounts: Multiple applications in a short time raise red flags.

- Errors on Credit Report: Wrong late payments or accounts.

- Employment Issues: Short job tenure or gaps.

How to Check Why You Were Denied

Lenders must send an adverse action notice (by law) explaining the reason. Review it carefully, then pull your free credit reports.

Step-by-Step Fixes to Get Approved Faster

- Fix Credit Report Errors (1-30 days impact): Dispute inaccuracies online via AnnualCreditReport.com. Common fixes add 20-100+ points.

- Lower Your DTI (Immediate-60 days): Pay down credit card balances or increase income. Target under 36%.

- Boost Credit Score Quickly:

- Pay all bills on time

- Reduce credit utilization below 30%

- Ask for credit limit increases (no hard pull)

- Strengthen Your Application: Gather strong proof of income and consider a co-signer.

- Choose the Right Lenders: Online fintechs (Upstart, Upgrade, Avant) are more forgiving than traditional banks.

- Wait Strategically: Space applications 30-45 days apart to avoid too many hard inquiries.

Best Lenders for Average Credit Borrowers (2026)

| Lender | Min. Score | APR Range | Funding Speed | Best Feature |

|---|---|---|---|---|

| Upgrade | 580 | 7.74%-35.99% | 1 day | Flexible terms |

| Avant | 550 | 9.95%-35.99% | Next day | Fast for fair credit |

| Upstart | 300+ | 6.2%-35.99% | 1-3 days | AI underwriting |

| Credit Unions | Varies | Lower rates | 1-5 days | Best rates if eligible |

Real-World Example

Applicant with 650 score and 45% DTI denied by bank. After paying down $2,000 in credit cards (DTI to 32%) and disputing one error (+35 points), they were approved by an online lender at 18% APR within 48 hours.

Prevention Tips for Future Applications

- Pre-qualify only (soft pulls)

- Have documents ready before applying

- Build emergency savings to reduce borrowing needs

- Monitor credit monthly

FAQ

- How long after denial can I reapply?

- Immediately with different lenders, but wait 30 days for the same one.

- Will denial hurt my score more?

- One hard inquiry has minor impact; multiple in short time hurts more.

- Can I get a loan the same day after fixing issues?

- Yes, with prepared documents and suitable online lenders.

Author: Grok, Financial Content Specialist | Data from NerdWallet, Bankrate, LendingTree (2026).

Disclosure: Informational only. Consult a financial advisor for personalized advice.